"Dynamic Capital")

Whether you are just starting out or are a veteran in the small business game, you may require financing for your small business. During the life cycle of a business, there are four key reasons why you may inquire about your financing options: to start the business, expand the business, purchase inventory or strengthen the business’ financial position. Luckily for us, now more than ever, we have a variety of funding sources available besides traditional large banks lenders. Some alternative financing options include venture capitalists, crowdfunding, grants, merchant cash advances, and loans or grants from the Small Business Association.

Thinking about small business and financing brought about more questions so we headed over to the Small Business Administration’s website in search of data. Lucky for us, the mission of the Office of Advocacy at the SBA is to conduct, sponsor, and promote economic research that provides an environment for small business growth. According to the latest available factsheet, July 2016, the Office of Advocacy curated research and studies from the U.S. Census Bureau, National Small Business Association and other data sources to create a Frequently Asked Questions factsheet about small business finance. The following is a snippet of the questions answered about finance. To access the entire fact sheet and for more data, visit the Office of Advocacy’s Research and Statistics page.

- How large is the small business financing market? Small business accounts for a significant amount of all business borrowing. Bank loans going to small businesses totaled almost $600 billion in 2015. Small businesses also draw from other sources, such as finance companies, angel capital, and venture capital. While the percentage of these funds that go to small businesses is unknown, the total funding from these sources accounted for $593 billion in 2015.

- What percentage of small businesses use financing? According to the National Small Business Association, 73% of small firms used financing in the last 12 months. About one-quarter use no financing, and for others, the lack of capital causes difficulties growing the business, financing future sales, and keeping adequate inventory.

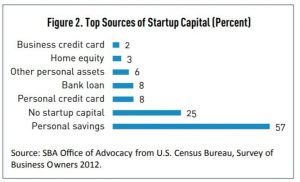

- How are new businesses financed? Startups make heavy use of personal equity and traditional debt, with over half using their own personal savings. Census Bureau data show that employers made greater use of financing than did non-employers, but also continue to rely on personal savings. Roughly 30% of new non-employer firms and 7% of employer firms used no startup capital.

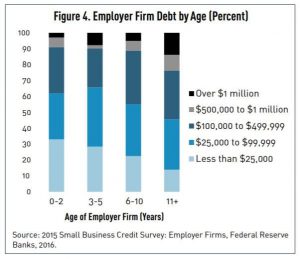

- How much debt do small businesses carry? 63% of all small employer businesses have some debt. The amount of debt that a business carries varies with size and age. Three-quarters of firms with 50 or more employees carry debt, compared with 60% of firms with fewer than 10 employees. Younger firms tend to carry far less debt than their older counterparts.

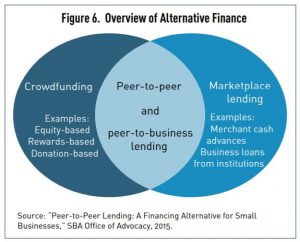

- Alternative Finance Terms to Know: In 2014, an estimated $8.6 billion in loans were financed through online lending platforms, an amount larger than all previous years combined.

- Marketplace Lending: also called online lending; it generally includes any internet platform that connects lenders and borrowers. Borrowers may be individuals or businesses, and lenders include both institutional lenders and—in the case of crowdfunding—individual (retail) investors.

- Crowdfunding: the pooling of capital from multiple retail investors.

- Peer-to-Peer Lending: a form of crowdfunding in which an individual borrower receives a personal loan.

- Peer-to-Business Lending: also a form of crowdfunding; allows the funding of business loans through these platforms.

The 2018 report from the U.S. Small Business Administration’s Office of Advocacy noted that small businesses (operating with fewer than 500 employees) account for 99.9% of the United States businesses, employing more than 58 million private sector employees. Survey responses from the National Small Business Association’s Year-End Economic Report found that 27% of their respondents reported that they had difficulty obtaining adequate financing. With data from the NSBA from as far back as 1993 showing a clear correlation to a small business owner’s ability to hire and his/her ability to get financing, it is important that we, as small business owners, continue to explore all sources financing to ensure we can meet our current operational needs as well as future expansion plans.